Term life insurance is a simple, temporary, and affordable way to protect your loved ones from financial disaster during your prime earning years.

Whole life insurance offers permanent coverage, builds cash value, and is more expensive than term.

If you’re wondering, “Do I need term or whole life insurance?” The best place to start is reviewing your finances and goals. In this guide, you’ll learn the differences between term and whole life insurance, and which is best for you.

What Is the Difference Between Term and Whole Life Insurance?

Life insurance policies fall into one of two categories: term and permanent. Among the various types of permanent life insurance options, all of which provide coverage for your entire lifetime, whole life insurance is a popular choice.

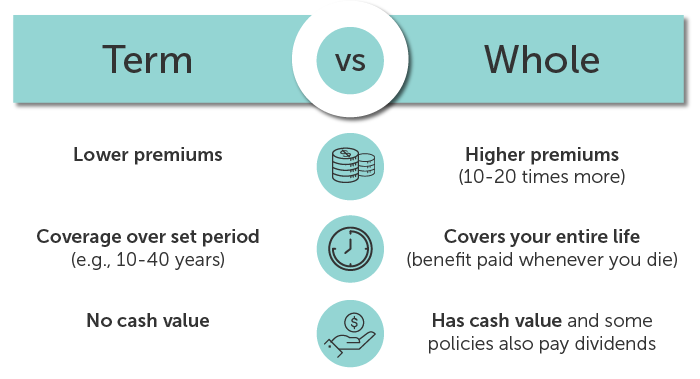

The main differences between whole and term life insurance are how long it lasts and the cost.

- Term life insurance lasts a specific length of time, e.g., 10-40 years, and pays a death benefit if you die during the term. Whole life insurance is lifelong and pays a death benefit no matter when you die.

- Term life insurance is basic financial protection for your beneficiaries. Whole life insurance protects your beneficiaries and accumulates cash value that you can access while living. Some whole life insurance policies also pay dividends.

- Term life insurance is affordable and can be customized to fit most budgets. Because of its features, whole life insurance is about 10-20 times more expensive than term.

Term Life Insurance

Term life insurance is temporary life insurance coverage. It’s designed to last for a set period and terminate when you no longer need it. Many people buy term life insurance when they get married or have their first child and choose a term length to carry them to retirement.

Term insurance is the most cost-effective and can be tailored to various budgets. Length options range from 10 to 40 years, and coverage amounts range from $50,000 to over $65 million. If you die within the active term period, the insurer will pay your beneficiary(ies) the policy’s death benefit.

When you buy a term life insurance policy, you lock in your rate for the entire term. Your price will stay the same as you age or encounter changes in your health.

Additionally, most term life insurance policies have conversion and renewal options built into the policy. These options are helpful if you decide you need life insurance but are now likely uninsurable.

Learn more about what happens if you outlive your term life insurance policy and your options to extend coverage.

Whole Life Insurance

Whole life insurance is life insurance coverage that lasts your entire life. As long as you keep your policy inforce, the life insurance company pays your beneficiary(ies) the policy’s death benefit no matter when you die.

Whole life insurance also has a cash value component that steadily grows over time at a fixed rate. Once you’ve built up enough value, you can borrow against your policy in the form of loans.

There are pros and cons to this, though. The policy loan accrues interest and reduces your death benefit unless you pay it back.

Whole life insurance is typically about 10-20 times more expensive than term. This is because of its lifelong coverage, savings component that builds cash value, and dividends.

Whole life insurance coverage varies from $10,000 to over $65 million. This is the amount your beneficiaries receive upon your death.

As far as permanent life insurance plans go, whole life insurance is one of the least complicated.

Other permanent life insurance plans include:

- Guaranteed Universal Life: The simplest form of permanent life insurance. It’s cheaper than whole life because it doesn’t offer much cash value potential—an excellent option for families who need lifelong coverage but can’t afford whole life insurance premiums.

- Universal Life: Features include flexible premiums and the option to increase your death benefit. Cash values fluctuate with market interest rates.

- Indexed Universal Life: Similar to universal life insurance, but cash values are tied to a stock market index. With an IUL, there’s more risk and potential for more reward compared to previously mentioned types of permanent life insurance.

- Final Expense: Type of permanent life insurance for which you can’t be turned down if you’re 50 to 80 years old. There are no medical questionnaires or exams. Final expense policies have small coverage amounts, often between $2,000 and $25,000, yet have high premiums due to the guaranteed acceptance factor. It’s often referred to as last resort life insurance.

Unsure which type you need? Contact our experts to learn more about whole life and term life insurance policies.

See what you’d pay for life insurance

Term vs Whole Life Insurance: Pros and Cons

Here’s a quick summary of the features of term and whole life insurance.

Term Life Insurance

Pros:

- Affordable

- Level premiums

- Many term length and coverage options

- Conversion and renewal options

Cons:

- Fixed level premium coverage expires

- Expensive to convert or renew later on

- No refunds when policy expires

Whole Life Insurance

Pros:

- Level premiums

- Cash value accumulation

- Potential dividend payouts

- Guaranteed payout to your beneficiaries

Cons:

- Very expensive

- Accessing the cash value has consequences

Term vs Whole Life Insurance: Which Is Better for You?

The main goal of life insurance is to protect your loved ones during their most financially-vulnerable years. In most cases, term life insurance makes the most economic sense since you only pay for coverage during those vital years.

However, whole life insurance has many benefits and can be the right choice in some circumstances. Let’s go over some scenarios to help you decide.

Guidelines for Choosing Term Life Insurance

If you have a young family and a mortgage, your loved ones are in their most financially susceptible years. Your spouse and children depend on your income. If you were to die suddenly, would they be affected financially? This is where term life insurance can be indispensable.

Are you on a budget?

If you want a budget-friendly policy, term life insurance is ideal because it’s inexpensive.

A small $100,000 life insurance policy can go a long way for a struggling family, and its premiums are competitive. Even if you’re not in stellar health, a $100,000 policy is affordable.

Do you have outstanding loans?

Term life insurance is sensible if you have loans because you can dictate how long you want coverage.

For example, let’s say you and your spouse just purchased a house for your growing family. Your mortgage loan is a 30-year term. Buying a 30-year term policy makes the most sense. It will be the financial backup should you die unexpectedly and ensure your family won’t have to sell the house.

Term life insurance is an affordable way to protect your family from any debt they may be responsible for upon your death.

Are you a good saver?

If you’re a good saver, purchasing term life insurance to protect your family for an absolute number of years is beneficial. Your family has the protection they need when they need it. The protection drops off later in life when your children are grown, the mortgage is paid, and you have healthy retirement savings built-up.

Like many types of insurance, term life insurance is a product you hope you never have to use.

When to choose term life insurance:

- If you need affordable coverage.

- If you have young children.

- If you have a spouse or partner relying on you.

- If you have debt.

- If you’re working on saving for retirement.

Guidelines for Choosing Whole Life Insurance

Whole life insurance can be expensive. But if you can afford the premiums, it can be beneficial to have in your portfolio.

Do you have a child with special needs or a disability?

If you have dependents who rely on you long-term, then a whole life policy is best. However, if lifelong dependents are the only reason you’re considering whole life, guaranteed universal life insurance may be the better choice because it’s less expensive.

Do you have a large estate?

Whole life insurance can benefit your heirs if your estate is worth millions of dollars. They can use the death benefit to pay estate taxes, so they’re not forced to sell valuable or sentimental assets.

Do you own a business?

Life insurance is helpful for business owners in many ways. It can be used to pay off heirs in a buy-sell agreement so your business can continue to run successfully.

If it’s a family business, you can use whole life insurance to provide an inheritance for children uninterested in the family business.

Are you not a disciplined saver?

You may have heard the saying, “Buy term and invest the difference.” Because term insurance is so affordable, it makes sense to own term and put the money you would have spent on a whole life policy into investments. However, this only works if you actually invest that difference.

Consider a whole life policy if you make a good income and just let it sit in a checking account instead of putting it to work. It will accumulate cash value and ensure you leave your family money to pay end-of-life expenses.

When to choose whole life insurance:

- You have a large estate.

- You own a business.

- You have a child who will always depend on you financially.

- You’re wealthy and have extra disposable income.

The table below provides an idea of the difference in term and whole life insurance pricing. The example applicant is a healthy, non-smoking man paying monthly premiums.

It’s important to note that when it comes to life insurance, you have options. Individuals can have a mix of both types, and for couples, it’s entirely acceptable to choose different coverage plans.

Recently, Business Insider featured insights from insurance expert Eleanor Johnson, CPA, CLU, CGMA, who is the founding principal of Highland Capital Brokerage. She recounted an interesting case involving a couple she assisted. The husband leaned towards cost-effective term life insurance, while the wife believed that whole life insurance was a better fit.

Johnson emphasized a key point – couples don’t necessarily need to see eye to eye on the type of life insurance; what matters is acknowledging the need for it. She highlighted, “If one wants term insurance and the other whole, that’s fine, as long as they understand what their policy could provide for them and their family in the future. The key is buying the amount of coverage that you need.”

How Much Term or Whole Life Should I Get?

Whether you buy term, whole, or a little of both is ultimately up to you. How much to get depends on your lifestyle and financial situation.

We recommend using term life insurance to cover things that won’t always need your financial focus, e.g., your mortgage, credit card debt, children’s standard of living, and education—the big-ticket items.

Choose a term length long enough to protect your family until all or a majority of your debt is paid off. Choose the most comprehensive coverage that you can comfortably afford.

If you need life insurance coverage until the day you die—no matter when that may be—we recommend buying a whole life insurance policy to supplement the more significant term policy.

Because many other better investment tools are available, it doesn’t make fiscal sense to buy large amounts of whole life insurance. But a small whole life insurance policy can supplement a larger term life insurance policy.

Use our Term Life Calculator to quickly and simply discover how much term life insurance coverage you need.

Explore Quotacy’s Life Insurance Options and Expert Advice

There is no question. If you can only afford term life insurance, that is the best option.

If you have a solid financial portfolio and are looking for more ways to supplement your retirement funds, have a business, or need life insurance that lasts your entire life, whole life insurance may be the way to go.

If you aren’t sure, Quotacy can help. Our non-commissioned agents will offer unbiased advice and advocate for you.

If you’re interested in term life insurance, getting a term quote is simple, easy, and only takes a few seconds. You don’t even need to provide any contact information to see quotes.

If you’re more interested in getting whole life insurance quotes, complete the form, and an agent will reach out to schedule a call. Because of the complexities of whole life insurance, we find that a quick phone call helps to ensure you’re getting a policy that meets your financial needs.

Note: Life insurance quotes used in this article are accurate as of October 17, 2023. These are only estimates and your life insurance costs may be higher or lower.

55 year old woman who needs life insurance outside my job. Can I get a good rate. Want to use for death benefits and pay off my home.

After the 20 year term does the life insurance lose it’s value (term)?

Hi Rachel, it’s very smart to get life insurance outside of your job. To be clear, a 20-year term life insurance policy would only provide a death benefit if you were to die during those 20 years. If you do not renew the policy or convert it, your coverage will terminate at the end of the 20-year term.

A term policy is useful to protect loved ones that depend on you. For example, if you have a partner or children who live in your home with you, it helps them continue to live in the home if you were to die unexpectedly. Term life insurance is not an investment tool that provides a guarantee payout.

You can quickly get estimates for a term life insurance policy through our quoting tool here: term life insurance quotes.

I’m a 60yr.old woman. I receive disability and social security supplement. It’s in the poverty level income. I want to leave something for my 2 children. What is my best choice term or whole life insurance.

Hi Elizabeth – I suggest that you call (844) 786-8229 or text (612) 260-4575 a Quotacy advisor. We’d be happy to go over your individual needs and recommend a policy that fits in your budget.

Does term life have a cash value when it is termed

Hi Christine, no term life insurance policies do not accumulate cash value like permanent life insurance policies.